The 20% loss in your “safe” bond fund wasn’t an accident; it was the result of a decade of financial distortions finally unwinding.

- Long-duration bonds, once seen as stable, acted like leveraged bets against rising rates, causing amplified losses.

- The traditional safety net of stock/bond diversification failed as correlations flipped positive, meaning both asset classes fell together.

Recommendation: Rebuilding your portfolio requires moving beyond simple diversification and focusing on actively managing duration risk and understanding real yields to build true resilience.

If you’re reading this, you likely experienced a shock in 2022. Your bond portfolio, the bedrock of a defensive strategy, suffered losses that felt more appropriate for a volatile tech stock. You were told bonds were “safe,” the counterbalance to equity risk. Yet, when inflation surged and central banks hiked rates, that safety net unraveled, leaving many investors with losses of 20% or more. The pain and confusion are understandable. You followed the rules, but the game changed completely.

The standard explanations—that bond prices and interest rates have an inverse relationship—are true, but they feel hollow. They don’t capture the sheer violence of the market move or explain why this time was so different. They don’t address the breakdown of the classic 60/40 portfolio, where bonds failed to protect investors from falling stock prices. The truth is more complex. Your portfolio wasn’t just a victim of rising rates; it was a casualty of a financial machine distorted by a decade of quantitative easing and zero-interest-rate policy.

This article is the autopsy of that failure. As a fixed income manager, my goal is not to dwell on the losses, but to dissect the mechanics of what happened. We will move beyond the platitudes to explore the hidden risks in duration, the illusion of safety in index-linked gilts, and the systemic regime shift that caught so many by surprise. More importantly, this analysis will form the blueprint for rebuilding. By understanding why the old model broke, you can construct a more resilient bond allocation for the new, and more volatile, financial era that lies ahead.

To navigate this new landscape, we will break down the key questions and challenges facing every bond investor today. This guide provides a structured path from understanding the mechanics of the loss to building a forward-looking strategy.

Summary: Why Did Your “Safe” Bond Fund Lose 20% When Interest Rates Rose?

- Why Does a 1% Rate Rise Cause a 10% Loss in Long-Duration Gilts?

- How to Generate 5% Yield from Bonds Without Taking 10-Year Duration Risk?

- UK Gilts vs Investment-Grade Corporate Bonds: Which Offers Better Value After Rate Rises?

- The Index-Linked Gilt Purchase That Lost Money Despite 10% Inflation

- When to Extend Duration: Before or After the Bank of England Signals Rate Cuts?

- Why Does Quantitative Easing Inflate Asset Prices While Wages Stagnate?

- Why Do Stock-Bond Correlations Flip from Negative to Positive During Inflation Spikes?

- Why Did UK Property Prices Rise When the Economy Shrank During the Pandemic?

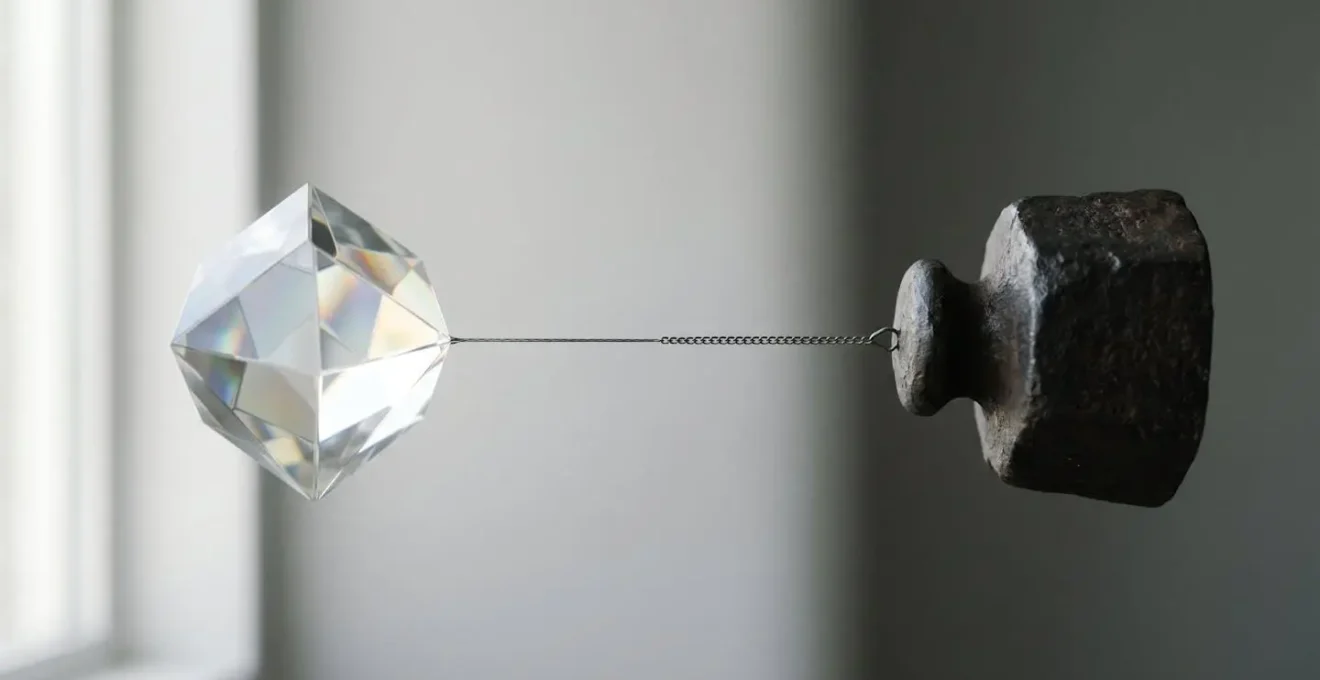

Why Does a 1% Rate Rise Cause a 10% Loss in Long-Duration Gilts?

The core of the pain felt by bond investors lies in a concept called duration. In simple terms, duration is a measure of a bond’s sensitivity to interest rate changes. A bond with a duration of 10 years is expected to fall approximately 10% in price for every 1% rise in interest rates. For years, in a low-rate world, investors were encouraged to buy longer-duration bonds to capture slightly higher yields, unknowingly turning their “safe” holdings into a leveraged bet against rate hikes.

This risk is not linear. A secondary effect, known as convexity, means that as rates rise and prices fall, the price decline can accelerate. This is precisely what happened during the 2022 UK gilt market crisis. The market wasn’t just reacting to inflation; it was grappling with a sudden, violent repricing of duration risk that had been suppressed for years. Detailed analysis from the Bank of England on the 2022 gilt crisis revealed how selling pressure from leveraged investors created a self-reinforcing downward spiral, particularly in long-dated gilts.

As the image metaphorically suggests, the descent started gradually and then became progressively steeper. This is the effect of negative convexity at play, where the initial losses make the portfolio even more sensitive to further rate moves. Investors who thought they held a simple, low-risk asset discovered they were exposed to a dynamic that could generate rapid, accelerating losses far beyond what they had ever anticipated. Understanding duration isn’t just academic; it’s the key to understanding exactly where the 20% loss came from.

How to Generate 5% Yield from Bonds Without Taking 10-Year Duration Risk?

After the shock of 2022, the idea of holding long-duration bonds is understandably unnerving. However, the silver lining of higher rates is that meaningful income has returned to the bond market. The challenge is capturing this yield without re-exposing your portfolio to the same duration risk. One effective portfolio construction technique for this environment is the bond barbell strategy.

A barbell strategy avoids intermediate-maturity bonds (e.g., 3-9 years) and instead concentrates holdings at the two extremes: the very short end and the long end. The short-term bonds (e.g., 3 months to 2 years) provide liquidity, stability, and the ability to reinvest at higher rates if central banks continue hiking. The long-term bonds (e.g., 10+ years) provide a higher starting yield. This structure gives you a blended yield and duration, but with more flexibility than a simple “bullet” portfolio concentrated in the middle.

The primary benefit is strategic flexibility. If you believe rates will continue to rise, you can let your short-term bonds mature and reinvest the proceeds into new, higher-yielding short-term paper. If you believe rates are peaking and cuts are on the horizon, you can begin to sell your short-term holdings and add to the long end to lock in yields and benefit from price appreciation. It’s a more active approach, but it puts you back in control of managing duration risk in a volatile world.

Your Action Plan: Building a Bond Barbell

- Determine Allocation Split: Begin by dividing your bond allocation between the short and long ends, for example, a 60/40 split between short-term bonds (0-2 years) and long-term bonds (10+ years), avoiding the middle.

- Select Short-Term Instruments: Collect your short-term holdings. This can include individual Treasury bills, high-quality corporate bonds maturing within two years, or liquid short-term bond ETFs.

- Choose Long-Term Positions: For the other end of the barbell, select long-term government or investment-grade corporate bonds that offer an attractive yield to lock in for the future.

- Monitor and Rebalance: As your short-term bonds mature, assess the interest rate environment. Reinvest the proceeds into new short-term bonds if you expect rates to stay high or rise, or reallocate to the long end if you anticipate rate cuts.

- Adjust Barbell Weights: Review the overall split between the short and long ends quarterly. You can dynamically shift the weighting based on your evolving view of the economic cycle and central bank policy.

UK Gilts vs Investment-Grade Corporate Bonds: Which Offers Better Value After Rate Rises?

With yields now at attractive levels, the next decision is where to allocate: to the perceived safety of UK government bonds (gilts) or to the higher-yielding, but higher-risk, world of investment-grade corporate bonds? The 2022 sell-off was indiscriminate, hitting both asset classes hard; data from MSCI shows the UK investment-grade corporate bond index fell a staggering 19.11%.

The key metric for comparing them is the credit spread – the extra yield (or “spread”) that a corporate bond offers over a government bond of the same maturity. This spread is the compensation an investor receives for taking on credit risk (the risk the company defaults). When spreads are wide, corporate bonds are considered cheap relative to gilts. When spreads are narrow, they are considered expensive, and you aren’t being paid much to take on the extra risk.

Making a decision requires a nuanced view that goes beyond just looking at the headline yield. The following table breaks down the current strategic considerations for a portfolio manager weighing these two options, based on an in-depth comparative analysis of credit spreads.

| Metric | Current Assessment | Key Insight |

|---|---|---|

| Corporate bond spreads vs gilts | Near 5-year lows | Corporate bonds appear expensive relative to gilts |

| Corporate bond spreads vs swaps | More neutral valuation | Gilts have cheapened relative to swaps due to high supply and QT |

| Credit spread drivers | Three structural factors | Record UK government spending, BoE quantitative tightening, reduced pension demand |

| Investment recommendation | Neither attractive nor unattractive | Strategic allocation objectives should guide decisions over tactical timing |

The takeaway is that there is no simple answer. While gilts offer lower default risk, their prices are sensitive to factors like government supply and central bank actions. Corporate bonds offer higher yields, but with spreads at historically tight levels, investors must be selective. The right choice depends on an investor’s overall portfolio objective and risk tolerance rather than a simple tactical bet.

The Index-Linked Gilt Purchase That Lost Money Despite 10% Inflation

Perhaps the most counter-intuitive and painful experience for defensive investors was the performance of index-linked gilts (or “linkers”). These were marketed as the ultimate protection against inflation, with both their principal and coupon payments increasing with the Retail Prices Index (RPI). Yet, in 2022, as inflation soared past 10%, the FTSE All-Stocks Index-Linked Gilt index collapsed by a stunning 33.6%. How could an asset designed to protect against inflation lose a third of its value during one of the worst inflationary spikes in a generation?

The answer lies in the distinction between inflation compensation and real yield. The total return of an index-linked bond comes from two sources: the uplift from inflation, and the price change from moves in its real yield. For very long-duration linkers, the second factor is overwhelmingly dominant. A rise in the real yield demanded by the market can create a capital loss that completely wipes out, and even dwarfs, the benefit of the inflation accrual. The flawed assumption was that “inflation-linked” meant “price-protected.”

This dynamic is perfectly illustrated by the case of the 50-year inflation-linked gilt maturing in 2073. As real yields rose from deep negative territory towards positive levels in 2022, this single bond experienced a catastrophic capital loss of 60.9%, according to analysis by Artemis Funds. The inflation uplift was a drop in the ocean compared to the tsunami of the real yield shock. This demonstrates that these instruments are not simple inflation hedges; they are complex duration instruments whose primary driver is the movement in real, not nominal, interest rates.

When to Extend Duration: Before or After the Bank of England Signals Rate Cuts?

Having navigated the wreckage, the forward-looking question becomes one of timing. Locking in the currently high yields for a longer period—extending duration—is tempting, as it offers the potential for significant capital gains when central banks eventually pivot to cutting rates. Get the timing right, and you could see a repeat of past bond bull markets. Get it wrong, and you risk further capital losses if rates stay higher for longer. The crucial question is: do you move before or after the official signal?

History shows that bond markets are forward-looking. They don’t wait for a central bank’s press conference. Markets typically price in rate cuts 6-9 months in advance, meaning the biggest price gains often occur well before the first official cut is announced. Waiting for the “all-clear” signal from the Bank of England or the US Federal Reserve likely means you have already missed the most profitable part of the move. The majority of the price appreciation will have already happened.

However, moving too early is also perilous. A premature pivot to long duration in an environment of persistent inflation could lead to a repeat of 2022’s losses. The decision to extend duration, therefore, becomes a strategic one based on reading the economic data—slowing growth, falling inflation prints, rising unemployment—rather than waiting for the final policy announcement. This is the calculated risk that bond portfolio managers must now weigh.

The Fed’s rate hikes ended the bull market in bond prices that had been running since 1982.

– Fidelity Investment Research, Bond Market Outlook 2023

This end of a 40-year cycle marks a new era. The decision is no longer a simple “buy and hold” but a dynamic assessment of whether the data supports the market’s pricing of future rate cuts. The risk of being early versus the risk of being late is the central dilemma for bond investors in the current regime.

Why Does Quantitative Easing Inflate Asset Prices While Wages Stagnate?

To understand the fragility that led to the 2022 crash, we must look at its cause: the decade-long policy of Quantitative Easing (QE). The stated goal of QE was to support the economy by lowering borrowing costs. However, its primary and most direct effect was the massive inflation of financial asset prices—stocks, property, and, ironically, bonds themselves.

QE works by central banks creating new money to buy government bonds from the open market. This has two effects. First, it pushes the price of these bonds up and their yield down, forcing investors seeking a return to buy riskier assets (the “reach for yield”). This bids up the price of corporate bonds, stocks, and other assets. Second, it floods the financial system with liquidity. This liquidity rarely flows directly into the pockets of workers in the form of higher wages; instead, it circulates within the financial system, chasing assets and inflating bubbles. Wages, on the other hand, are primarily driven by productivity, labour market tightness, and collective bargaining—factors largely disconnected from the direct mechanics of QE.

The policy created a generation of investors who had only ever known a world where central banks backstopped markets. But it came at a cost. When inflation finally returned, the unwinding of QE—known as Quantitative Tightening (QT)—and the rapid rise in interest rates revealed the true cost of this policy. For the government, this meant debt interest costs soared to £7.6 billion in a single month in mid-2022, as shown by ONS data. For investors, it meant the very foundation of their portfolio—the low-risk bond—had its price propped up by an artificial force that was now being removed.

The Fed had been financially repressing savers, especially retirees.

– Lisa Emsbo-Mattingly, Managing Director of Asset Allocation Research, Fidelity Bond Market Outlook

Why Do Stock-Bond Correlations Flip from Negative to Positive During Inflation Spikes?

The ultimate failure of the “safe” portfolio in 2022 was the breakdown of its core diversification principle. For decades, the 60/40 portfolio (60% stocks, 40% bonds) worked because stocks and bonds had a negative correlation. When stocks fell due to a “growth shock” (a recession), central banks would cut interest rates, causing bonds to rise in price and cushion the portfolio. This relationship was the bedrock of modern portfolio theory.

In 2022, this relationship shattered. The shock was not one of growth, but of inflation. High inflation forced central banks to do the opposite of what they’d do in a recession: they had to hike interest rates aggressively. This created a “common discount rate” shock. The value of a stock is the present value of its future earnings, and the value of a bond is the present value of its future coupons. When the interest rate (the discount rate) used to calculate that present value shoots up, it hammers the value of *both* assets simultaneously. The hedge failed.

This wasn’t a temporary blip; it was a full-blown regime shift. According to analysis from Morningstar on the 2022 correlation regime shift, the year marked a dramatic change where the traditional diversification benefit vanished. This event demonstrated that stock-bond correlation is not a fixed law of finance but is instead regime-dependent. In a low-and-stable inflation regime, the negative correlation holds. In a high-and-volatile inflation regime, it can flip to positive, with disastrous consequences for unprepared investors.

The key lesson is that the role of bonds as a diversifier is conditional. It works during growth shocks but fails during inflationary shocks. For investors rebuilding their portfolios, this means they can no longer blindly rely on a simple 60/40 split. They must now consider the inflationary environment and seek out assets or strategies that can provide true diversification during an inflation spike, a role that bonds temporarily abdicated.

Key Takeaways

- The “safety” of bonds is not absolute; long-duration bonds carry significant, levered risk to rising interest rates.

- The traditional diversification of a 60/40 portfolio can fail during inflationary shocks when stock-bond correlations turn positive.

- Building a resilient portfolio today means actively managing duration, understanding the drivers of real yield, and not blindly relying on past correlations.

Why Did UK Property Prices Rise When the Economy Shrank During the Pandemic?

The same forces that distorted the bond market also had a profound and seemingly paradoxical effect on other asset classes, notably UK property. During the pandemic, the UK economy experienced its sharpest contraction on record, yet house prices surged. This disconnect can be traced back to the same root cause: the unprecedented monetary and fiscal response, including QE and rock-bottom interest rates.

Ultra-low borrowing costs made mortgages cheaper than ever, dramatically increasing purchasing power. Simultaneously, policies like the Stamp Duty holiday acted as a direct fiscal accelerant to housing demand. This wasn’t a phenomenon driven by a strong underlying economy or wage growth; it was a classic asset bubble inflated by cheap credit and government stimulus. It was another symptom of the “everything bubble” where central bank liquidity, with nowhere else to go, flowed into any asset with a yield or a prospect of capital appreciation.

QE makes safe bonds scarce and low-yielding, forcing large investors like pension funds to move money into riskier assets to meet their return targets, thereby bidding up their prices.

– Investment analysts, Corporate bond market analysis

This illustrates the portfolio effect of QE. While the quote refers to financial investors, the principle applies to individuals too. With savings accounts paying zero, bonds yielding next to nothing, and a cultural belief in property as a one-way bet, capital flooded into the housing market. The 2022 rate shock was the moment this logic went into reverse. Just as rising rates crushed bond prices, they are now putting extreme pressure on the very foundation of the pandemic-era property boom, demonstrating that no asset class was truly immune to the eventual unwinding of these massive distortions.

The events of 2022 were a painful but necessary stress test for every defensive portfolio. The losses exposed the hidden risks baked into the market after a decade of unconventional policy. The key lesson is that the financial regime has changed. The old rules of “safe” assets and simple diversification no longer apply without question. Building a truly resilient portfolio for the future requires a more sophisticated approach: actively managing duration, demanding compensation for credit risk, and understanding that the correlation between asset classes is not a constant. It’s time to move from being a passive holder of assets to an active manager of risk. This is the blueprint for not just surviving, but thriving in the new era of investing.